From Invisible Hand to Helping Hand: GST and the Service Sector

Published on: Wed Apr 10 2024

Kapil Sharma

Bio (Reveal/Hide)

From Invisible Hand to Helping Hand: GST and the Service Sector

The implementation of the Goods and Services Tax (GST) in India in 2017 marked a significant reform in the country's indirect tax landscape. While the impact of GST on the manufacturing and trading sectors has been extensively analyzed, the implications for the vibrant service sector warrant equal attention.

The service sector contributes over 55% to India's GDP and is a key driver of economic growth. Understanding the intricacies of GST applicability, compliance requirements, and its overall impact on various service industries is crucial for businesses to navigate the new tax regime effectively.

History of GST and the Service Sector

Before the implementation of GST, the service sector in India was subject to a complex web of indirect taxes, including Service Tax, Value Added Tax (VAT), and various other levies.

This fragmented tax structure often resulted in the cascading of taxes, leading to a higher effective tax burden on service providers and consumers.

The introduction of GST aimed to simplify the indirect tax framework by subsuming multiple taxes into a single, comprehensive levy. This shift towards a destination-based consumption tax was expected to enhance transparency, improve ease of doing business, and facilitate seamless input tax credit (ITC) claims across the value chain.

How does GST work in the service sector?

- Destination-Based Taxation: Under GST, the place of supply determines the applicable tax jurisdiction and rate, unlike the earlier origin-based service tax regime.

- Tax Slabs for Services: Services are taxed at four primary rates under GST: 5%, 12%, 18%, and 28%, with specific exceptions and exemptions.

- Input Tax Credit (ITC) in Services: Service providers can claim ITC on the GST paid on procurement of input goods and services, subject to certain conditions.

- Reverse Charge Mechanism (RCM): Recipients of specified services from unregistered suppliers are required to pay GST under the reverse charge mechanism.

- Exemptions and Composition Scheme: Certain services are exempt from GST, while the composition scheme is available for small service providers.

- E-Invoicing and Compliance: Mandatory filing of GSTR-1 and GSTR-3B returns, along with the introduction of e-invoicing, have increased the compliance burden for service providers.

What are the benefits of GST for service providers?

- Input Tax Credit (ITC): The ability to claim ITC on input goods and services has helped service providers reduce their overall tax costs and improve profitability.

- Elimination of Cascading Effect: GST's single-levy structure has eliminated the cascading of taxes, leading to a more efficient and transparent tax system.

- Simplified Tax Structure: Consolidation of multiple indirect taxes into a single GST has simplified compliance and reporting requirements for service businesses.

- Expanded Tax Base: Bringing more service providers under the formal tax net has widened the overall tax base and improved revenue collection for the government.

What is the GST limit for the service sector?

The GST registration threshold for service providers is set at an annual turnover of ₹20 lakhs (₹10 lakhs for special category states). However, certain services, such as restaurant services, are subject to a lower registration limit of ₹40 lakhs.

Who will pay GST for services?

In general, the service recipient is liable to pay GST, except for a few cases where the service provider is responsible for charging and remitting the tax. The specific provisions for GST payment depend on the nature of the service and the status of the supplier and recipient.

What are the common challenges faced by service providers under GST?

- Frequent Changes in Rules: Numerous amendments in GST laws and procedures since implementation have increased the complexity for service providers.

- Input Tax Credit Restrictions: Denial of ITC on certain services, such as food, entertainment, and insurance, has raised the effective tax burden.

- Refund Delays: Delays in obtaining GST refunds, especially for exporters of services, have impacted working capital.

- Reconciliation and Documentation: Maintaining detailed records and reconciling ITC claims with supplier invoices have increased the administrative burden.

- Technical Glitches: Frequent technical issues on the GST portal have disrupted timely compliance, leading to late fees and penalties.

Impact of GST on the Service Sector

The impact of GST on the service sector has been varied, with different industries experiencing diverse effects. Let's examine the impact on some key service sectors:

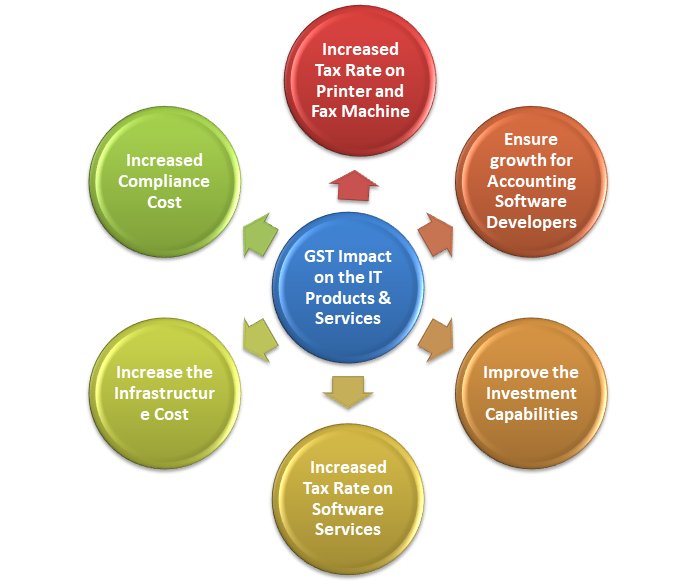

IT/ITeS

- GST rate reduced from 15% to 18% on most services

- Seamless ITC claim facilitates cost savings

- Compliance burden increased due to periodic return filing

Financial Services

- Banking, insurance, and stock broking taxed at 18%

- Restrictions on ITC claims for certain services

- Additional compliance for activities like the sale of mutual funds

Hospitality

- Room tariffs are taxed at 12% (up to ₹7,500) and 18% (above ₹7,500)

- ITC is available on procurement, reducing tax cascading

- Compliance complexity for maintaining detailed records

Real Estate

- Under-construction properties taxed at 12%

- Affordable housing projects at 8%

- ITC benefits for developers, impacting final prices

Healthcare

- Treatment services are exempt from GST

- ITC disallows procurement, increasing costs

- Compliance burden for ancillary services like diagnostics

Telecom

- Uniform 18% GST rate, replacing multiple levies

- ITC benefits, barring certain excluded services

- compliance burden increased due to periodic returns

Schedule of GST Rates for Services as Approved by the GST Council

Positive Effects of GST on the Service Sector

- Elimination of Cascading Effect: The seamless input tax credit mechanism under GST has helped service providers reduce the cascading of taxes, leading to a lower effective tax burden.

- Improved Competitiveness: The simplified tax structure and reduced compliance costs have enhanced the competitiveness of Indian service providers, especially in the global market.

- Expansion of Tax Base: Bringing more service providers under the formal tax net has widened the overall tax base, leading to improved revenue collection for the government.

- Ease of Doing Business: The consolidation of multiple indirect taxes into a single GST has simplified compliance and reporting requirements for service enterprises, improving the overall ease of doing business.

- Boost to Exports: The zero-rating of export services has enhanced the competitiveness of Indian service providers in the global market, leading to increased export opportunities.

- Technological Advancements: The need for efficient GST compliance has spurred the growth of specialized service providers, such as GST Suvidha Providers (GSPs) and Accounting Software providers, driving innovation in the sector.

Way Forward

To further enhance the benefits of GST for the service sector, the following measures can be considered:

- Rationalization of GST Rates: Convergence towards fewer tax slabs can simplify compliance and improve the overall tax structure.

- Seamless Input Tax Credit: Broadening the ITC scope and streamlining refund mechanisms can enhance liquidity and reduce the effective tax burden on service providers.

- Stabilization of GST Portal: Improving the technological infrastructure and user interface of the GST Network can facilitate smoother compliance and reduce disruptions.

- Capacity Building: Enhancing awareness and skill development initiatives for service providers can improve understanding of GST provisions and compliance requirements.

- Efficient Dispute Resolution: Establishing efficient grievance redressal mechanisms and increasing the judicial capacity of GST authorities can expedite the resolution of disputes.

By addressing these areas, the GST regime can unlock the full potential of the vibrant service sector and contribute to India's economic growth and development.

Related Posts