Central Board of Indirect Taxes and Customs (CBIC)

Published on: Fri Aug 30 2024

Aditya Singh

The Central Board of Indirect Taxes and Customs (CBIC): A Comprehensive Overview

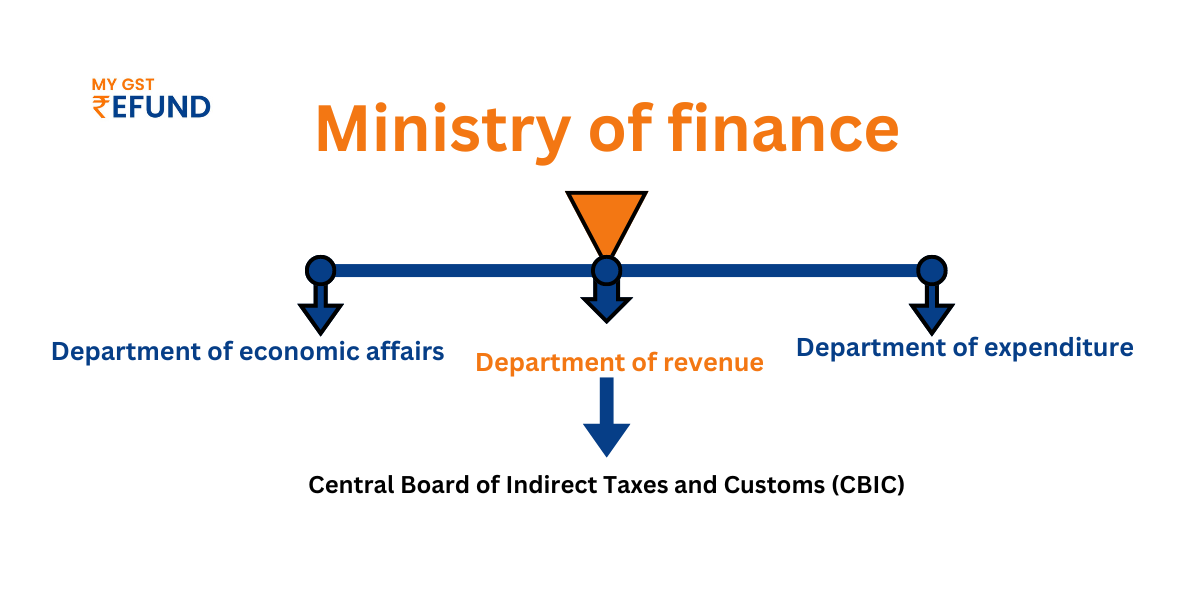

In the Indian Ministry of Finance, the Central Board of Indirect Taxes and Customs (CBIC) assumes a pivotal position as far as managing and regulating the indirect taxation system of the country is concerned. Originating from the colonial India era, today it plays a crucial role in administering indirect taxes like goods and services tax (GST), customs duties, and excise duties. This article explores its history, functions, institutional structure, roles, and major reforms.

1. Historical Background of CBIC

The Customs and Excise Department was created by the British Indian Government in 1855, thus marking the birth of CBIC. It initially focused on customs administration and import duty collection; however, over time it began to accommodate developments within the growing, diversified economy of India.

In 1964, after independence, India’s central board also went through restructuring when the Central Board of Revenue was divided into two divisions, namely the Central Board of Direct Taxes (CBDT) as well as the Central Board of Excise and Customs (CBEC). Such an overhaul made both direct taxes and indirect taxes more manageable on their own.

2. Functions of CBIC

The scope of functions of CBIC is wide, covering all kinds of indirect taxes in India. The major roles it plays include:

- Administration of Indirect Taxes: Collects and manages GST, duty on imports and exports, as well as excise throughout the whole country.

- Customs Regulation: This is done through enforcement of Customs Act 1962, ensuring that import/export regulations, tariffs and trade rules are duly complied with. It plays an important part in facilitating trade across borders while adhering to customs law.

- Anti-Smuggling Operations: One way in which CBIC helps is by fighting smuggling and other illegal activities that threaten to undermine the Indian economy. Some of these include putting stringent measures aimed at preventing the movement of illegal substances or goods.

- Policy Formulation: It also plays a very vital role when it comes to formulating different policies regarding indirect taxes, customs and excise duties. It implements these policies at the national level to ensure their effectiveness.

- International Cooperation: It works with various international customs organizations and tax authorities for smoother international trade, implementation of international treaties, as well as ensuring compliance with international trade norms.

- Dispute Resolution: CBIC is vested with the responsibility of resolving tax disputes and handling complaints pertaining to indirect taxes so that the same are rationalized.

3. Organizational Structure of CBIC

Organisational Chart of the Central Board of Indirect Taxes and Customs (CBIC)

The following is a comprehensive and hierarchical structure of CBIC that spans across India:

- Directorates: Several specialised directorates exist within CBIC, including the Directorate of Revenue Intelligence (DRI), the Directorate General of GST Intelligence (DGGI), and the Directorate General of Analytics and Risk Management (DGARM). These directorates manage specific areas such as enforcement, intelligence gathering, and risk management in tax matters.

- Field Formations: A network of field formations like zonal offices, commissionerates, or customs houses is included in the CBIC’s effective local administration system of indirect taxes.

- GST Commissionerates: With GST being implemented as a new tax regime, dedicated commissionerates were formed to manage its operations throughout India.

- Customs Houses: The customs houses administered by CBIC at major ports and airports take care of all customs clearances alongside ensuring adherence to import/export regulations.

- Central Excise Zones: They collect and administer central excise duties on products like tobacco and petroleum.

4. Roles and Responsibilities of CBIC

The CBIC engages in different activities under the Indian taxation system, such as:

i. Tax Collection and Administration: where it makes sure the efficient collection of indirect taxes that form the greater part of government revenue.

ii. Trade Facilitation: which involves simplifying customs procedures to facilitate international and domestic trade, thereby contributing to India's goal of making it easier to do business.

iii. Enforcement and Compliance: CBIC enforces tax laws, aiming at ensuring compliance and avoiding evasion, thus enabling integrity within the indirect taxation system.

iv. Policy Implementation: It plays an integral role in implementing taxation reforms, including those associated with GST, ensuring their smooth execution.

v. Dispute Resolution: Tax-related disputes are managed by the board, which provides legal advice and makes sure grievances are settled quickly and equitably by all parties concerned.

With emerging issues on taxation and customs, CBIC takes an interest in training her officers so that they are prepared for unforeseen challenges ahead that may arise from these two areas (indirect taxes).

5. Importance of CBIC

CBIC’s significance in India’s financial landscape is immense. Some of the key areas where CBIC makes a critical impact include:

- Revenue Generation: Majorly through the collection of GST, customs duties and excise duties, CBIC substantially contributes to the revenue receipt of the center, which is very vital for financing government programs, infrastructure projects and social welfare initiatives.

- Economic Stability: By ensuring compliance with tax laws and reducing tax evasion, CBIC plays a vital role in maintaining economic stability and promoting sustained growth.

- Ease of Doing Business: The initiatives of CBIC to reduce cumbersome customs and tax procedures have improved India’s ease of doing business ranking, hence making it attractive for foreign investors.

- Protection of National Interests: In terms of combating smuggling and implementing customs laws, CBIC is essential to safeguarding both India’s economy as well as its national security.

- Policy Reforms: One key area where CBIC spearheads tax reforms is in the implementation of GST, which simplified and enhanced efficiency in India’s tax system, making it easy revenue collection wise.

6. Major Changes and Reforms in CBIC

CBIC has made many changes over the years as a result of modifications to India’s taxation system. The key changes are:

- Introduction of GST in 2017: GST changed India’s indirect tax system by consolidating various forms of tax into one. This meant that CBIC took up implementation and management of GST, giving it more duties than before.

- Renaming from CBEC to CBIC (2018): The board’s renaming from CBEC to CBIC reflected its broader mandate, particularly after the introduction of GST, as it now oversees all indirect taxes.

- Customs (Amendment) Act, 2021: Over the years, the Customs Act has undergone several amendments since 1962. These amendments have included raising penalties for smuggling in customs, establishing special customs courts, and enhancing partnerships with enforcement agencies. However, there is a clause in the 2020 Customs (Amendment) Act that enables the government to formulate regulations on anti-smuggling measures.

- Faceless Assessment (2020): CBIC has used faceless assessment as a way to reduce physical contact between customs officials and importers or exporters. Consequently, this reform will help combat corruption, increase transparency and facilitate ease of doing business.

- Electronic Invoicing (2020): Another major step towards improved tax compliance while reducing fraud was the introduction of electronic invoicing under GST. This helps businesses generate standardized invoices, which are easy for tax administration purposes.

- Customs (Administration of Rules of Origin under Trade Agreements) Rules (CAROTAR), 2020: These rules are in place to ensure that imports under free trade agreements meet their origin requirements, thus preventing any misuse of those agreements.

- Digital Initiatives: To improve efficiency in tax administration, CBIC has come up with various digital initiatives like the Indian Customs EDI System (ICES) and the CBIC-GST mobile application.

- Anti-Smuggling and Enforcement Measures: Various amendments have also been made by CBIC aimed at strengthening its efforts towards anti-smuggling, including increasing penalties for smuggling offenses; establishing special Customs Courts; and enhancing partnerships with law enforcement agencies. The 2020 Customs (Amendment) Act, however, allowed making regulations regarding anti-smuggling measures by the government.

7. Challenges Faced by CBIC

Regardless of its achievements, the CBIC is facing numerous obstacles:

- Cross-Jurisdictional Complexity of GST Administration: Managing a large and intricate GST system over various compliance levels across states is a significant challenge.

- Hardship in Customs Regulations Enforcement: Smuggling, under-invoicing and mislabeling of goods are still major problems in customs matters.

- Technological adaptation: Keeping up with digital reforms such as faceless assessments, e-invoicing calls for continuous technological improvement and capacity building.

Conclusion

The Central Board of Indirect Taxes and Customs (CBIC) plays an important part in administering India’s indirect tax system. From its historical roots to present-day responsibilities, CBIC has evolved with the changing needs of the Indian economy. Being an extensive authority, CBIC contributes to revenue collection, economic viability, trade facilitation and national security. Recent reforms, mainly regarding GST and digital transformation, have made CBIC one of the modern tax authorities in India. Yet as India grows into a global economy, it will demand continual adaptation from CBIC towards emerging challenges and opportunities.

Also Read: Central Board Of Direct Tax[CBDT]

Related Posts